Market Update: Mortgage Rates Dip Amid Economic Concerns — What It Means for Los Angeles and Beverly Hills Real Estate

{kind=link}

Despite higher-than-expected inflation data, last week saw a modest dip in mortgage rates as investor sentiment shifted toward growing signs of economic softening. One key catalyst was the disappointing consumer confidence report, which came in significantly below expectations — a signal that consumers are growing increasingly wary about the financial outlook. For homebuyers and sellers in Los Angeles and Beverly Hills, this shift could bring new opportunities and challenges alike.

Inflation, the Fed, and What’s Next

The Federal Reserve’s preferred inflation gauge — the Core PCE Price Index — showed prices rose 2.7% year-over-year in May, slightly higher than April’s 2.6% increase and just above market forecasts. While this reinforces that inflation is proving stubborn, particularly as new tariffs threaten to drive costs higher, investors seem more concerned with signs that consumer and labor markets may be cooling.

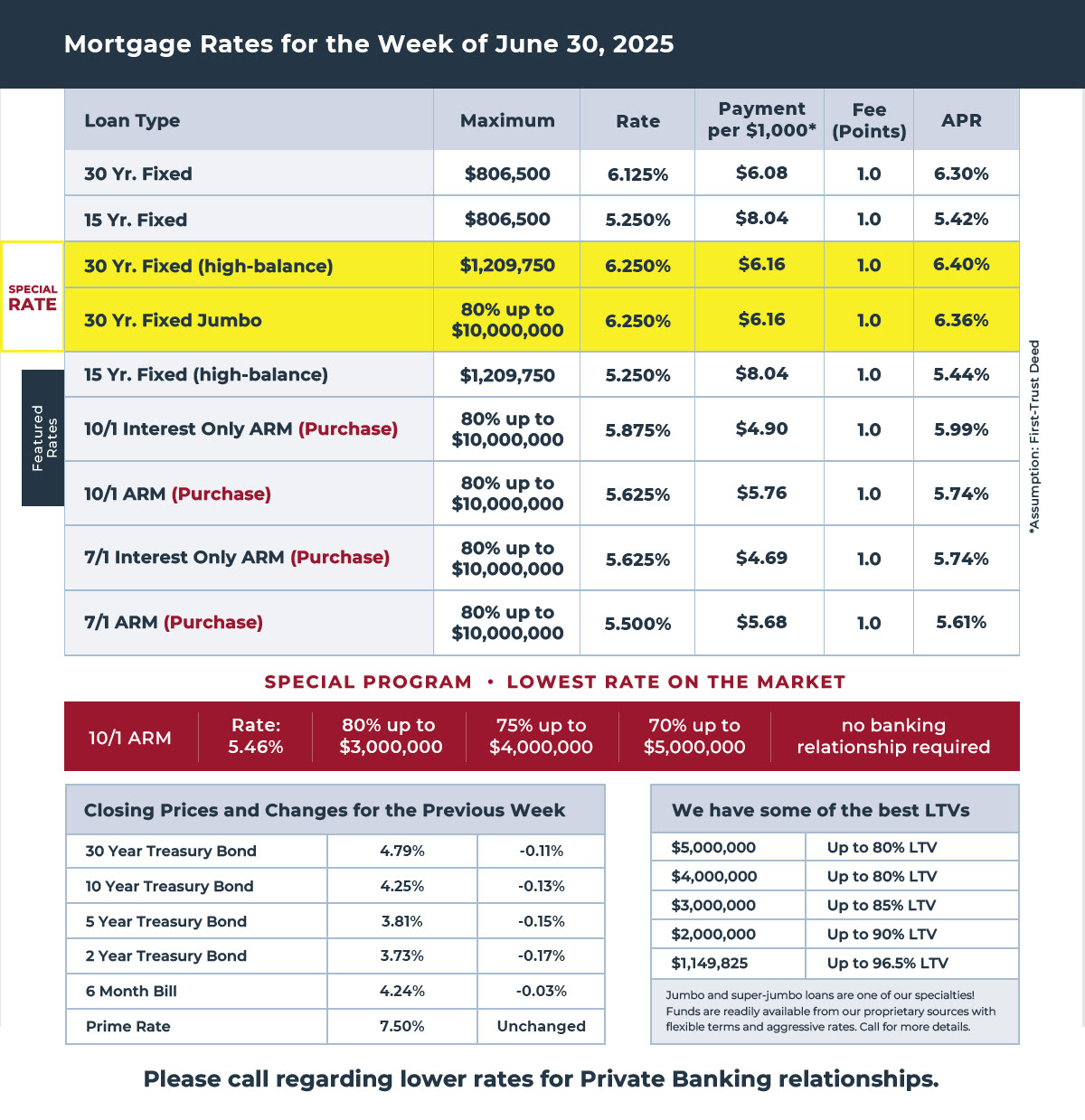

This shift in investor focus helped bring mortgage rates slightly lower by the end of the week, providing a potential window of opportunity for buyers in high-value markets like Beverly Hills, Bel-Air, Holmby Hills, and the Sunset Strip. For ultra-luxury buyers, even a minor rate change can represent significant savings or increased affordability.

Consumer Confidence and Job Outlook Falter

The Conference Board’s Consumer Confidence Index dropped to 93 in June — far below the expected 99 — with a noticeable dip in optimism across all age and income groups. Of particular concern: the perception of job availability and wage growth, both of which declined. These metrics are closely watched because housing decisions — especially in markets like Los Angeles, where price points are high — are closely tied to consumer sentiment and financial security.

National Housing Trends: Inventory Gains But Sales Lag

Nationally, May’s existing-home sales rose slightly from April, but remained at the slowest pace for the month since 2009. The median home price hit a record for May at $422,800, but was up only 1% from the prior year. Inventory increased to a 4.6-month supply — still below the 6-month norm for a balanced market but marking the highest level in five years.

In contrast, new home sales — a leading indicator since they are based on contract signings rather than closings — plummeted 14% from April. The median price of a new home was $426,600, up 3% year-over-year. These diverging trends suggest a cautious buyer pool and heightened sensitivity to pricing and economic uncertainty.

What This Means for Beverly Hills & Greater LA Real Estate

In Los Angeles’ luxury real estate market, we’re seeing a fascinating duality:

-

Inventory in high-end segments (particularly $10M+) has increased, giving buyers more choices than they’ve had in recent years.

-

However, seller expectations remain anchored to peak pandemic-era pricing, which can lead to longer days on market and necessary price adjustments.

-

Properties that are move-in ready, architecturally significant, or located in premium areas like The Bird Streets, Brentwood Park, and Trousdale Estates continue to see strong interest — particularly from international buyers and cash purchasers.

In Beverly Hills, buyers are becoming more discerning, taking their time to evaluate not just the property but also long-term economic factors. Sellers should take note: aligning your pricing with current data — not yesterday’s headlines — is essential to attracting offers in today’s evolving market.

Final Thought

For buyers, this moment may offer a rare mix of softened mortgage rates and growing inventory. For sellers, it’s a critical time to price strategically and market effectively to capture interest while uncertainty lingers.

Whether you're buying or selling in Los Angeles’ luxury real estate market, now is the time to work with a trusted advisor who can guide you through every nuance of this shifting landscape.