The One Thing You Can Influence: How to Control Your Rate This Season

{kind=link}

A Strategic Guide for Buyers Navigating Mortgage Rates in Beverly Hills and Los Angeles Luxury Real Estate

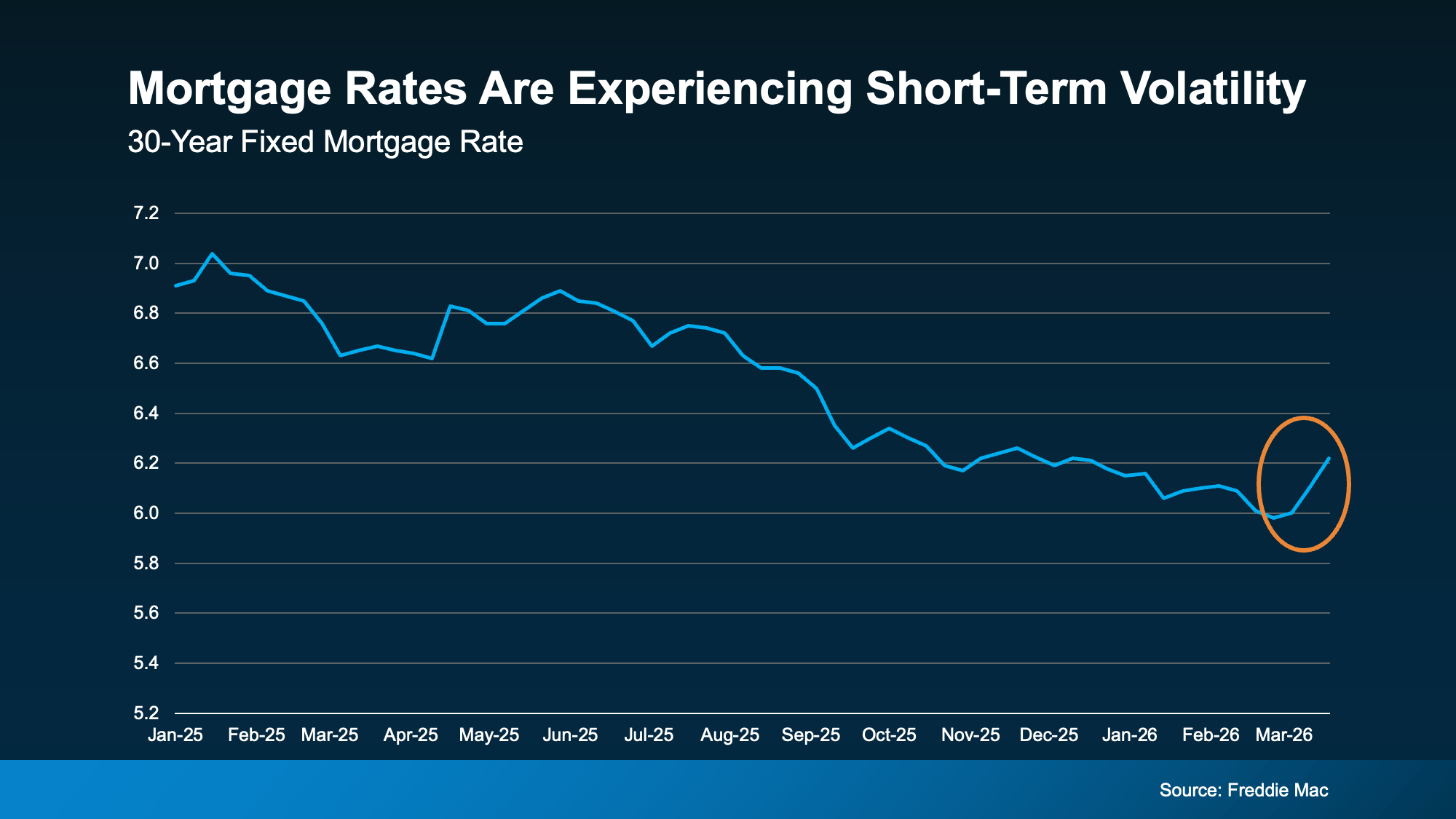

Mortgage Rate Volatility Is Part of the Market

Mortgage rates are moving. That is not new and it is not unexpected.

Recent data confirms that after a period of decline, rates have ticked upward again. What matters is understanding that these fluctuations are a normal part of the economic cycle, especially during periods of global uncertainty.

Mortgage rates continue to fluctuate in early 2026, reinforcing why strategic preparation matters more than timing the market.

Trying to perfectly time the market based on rates alone is rarely a winning strategy.

Focus on What You Can Control

While headlines may create hesitation, sophisticated buyers understand that success comes from controlling the variables within reach.

As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

There are three key levers that directly influence your mortgage outcome.

Your Credit Profile

Your credit profile is one of the most powerful tools in your financial positioning.

Even small improvements can meaningfully impact your rate and long term cost.

As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

Key considerations:

- Higher credit scores typically unlock more favorable rates

- Better loan terms often follow strong financial profiles

- Strategic credit adjustments can reduce lifetime interest significantly

Your Loan Structure

Not all loans are created equal. The structure you choose can dramatically affect both your rate and overall financial strategy.

The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

Loan options include:

- Conventional loans

- FHA and VA programs

- Jumbo financing for luxury properties

Each comes with distinct advantages depending on your profile and acquisition goals.

Your Loan Term Strategy

The length of your loan is not just a timeline. It is a financial strategy.

Common structures:

- 15 year loans for accelerated equity and lower interest

- 30 year loans for flexibility and liquidity preservation

- Custom structures tailored to wealth strategy

Freddie Mac offers this advice:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

The right choice depends on how you prioritize cash flow, leverage, and long term portfolio planning.

The Bigger Picture for Luxury Buyers

In the Beverly Hills and Los Angeles luxury real estate market, financing is not just about rates. It is about positioning.

Savvy buyers look beyond short term fluctuations and focus on:

- Asset appreciation potential

- Long term wealth preservation

- Strategic leverage in a dynamic market

Mortgage rates may fluctuate. Prime real estate opportunities do not wait.

“Luxury real estate decisions are not made by chasing rates. They are made by controlling strategy, timing, and opportunity.”

Bottom Line

You cannot control where mortgage rates go next.

You can control how well you are positioned to take advantage of the right opportunity when it appears.

Whether you are purchasing your first home or acquiring a legacy estate, preparation is your greatest advantage.

Cultivating the Right Partnership

Navigating these options requires more than just an algorithm; it requires a confidential consultation with a trusted lending professional who understands the intricacies of high-net-worth financing. By focusing on these internal metrics, you position yourself to act with confidence, regardless of the headlines.

Whether you’re selling next year or just giving your house some TLC... Let’s have a quick conversation about whether it’s the right decision for your home.

Contact Christophe Choo at (310) 777-6342 or [email protected] for a Confidential Property Valuation. To tour your future home and search communities click "HERE".