Waiting for Mortgage Rates to Drop? Read This First

{kind=link}

Should You Wait for Lower Mortgage Rates Before Buying?

Waiting for Mortgage Rates to Drop? The Math May Surprise You

Mortgage rates briefly dipped into the upper 5% range earlier this year before moving back into the low 6% range. For many buyers who caught that headline — and then watched rates tick back up — the reaction was immediate and familiar:

"I missed it."

You're not alone in feeling that way. But before you pause your search and wait for another dip, it's worth actually running the numbers. Because the difference may be far smaller than it feels.

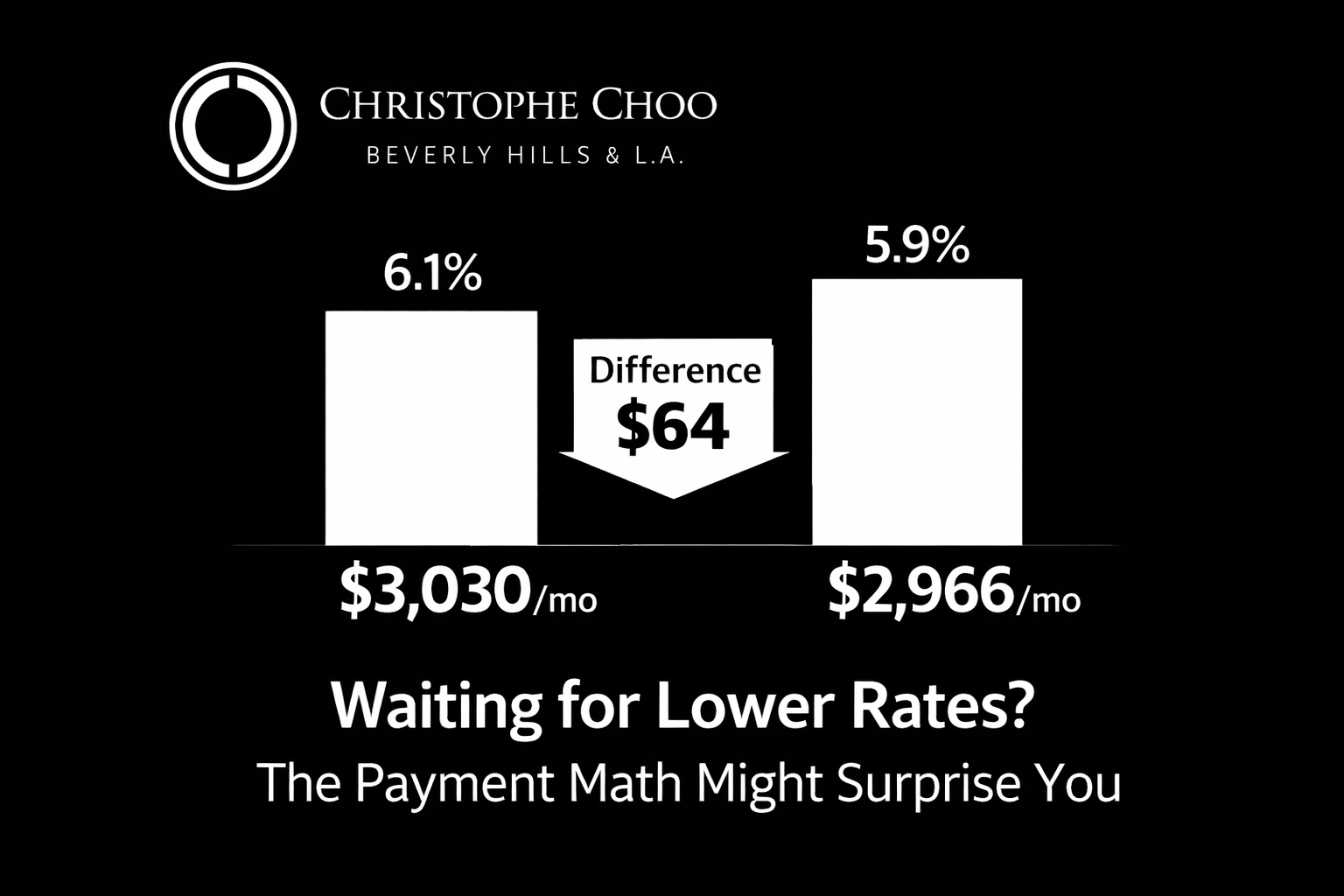

The Payment Gap Is Narrower Than You Think

Here's a straightforward comparison on a $500,000 loan:

- At 6.1%: Estimated principal and interest payment = $3,030/month

- At 5.9%: Estimated principal and interest payment = $2,966/month

The difference: approximately $64 per month.

Not hundreds of dollars. Sixty-four.

Over the life of the loan, those dollars compound — that's real money. But for most buyers weighing a purchase decision, the financial delta between 6.1% and 5.9% is not the decisive factor. What's actually driving hesitation is the psychological weight of the number itself. A "5" in front feels meaningfully different than a "6," even when the payments tell a subtler story.

The 5% Rate May Not Be Coming

It's worth being direct about what the forecasting landscape looks like: most housing economists are not projecting mortgage rates to settle into the 5% range in the near term. Rates will continue to fluctuate — occasionally brushing the high 5s — but the prevailing expectation is that we'll hover around the low-to-mid 6% range for the foreseeable future.

Waiting for a sustained drop into the 5s may mean waiting considerably longer than you expect. And the market you're waiting for may not hold the inventory, pricing, or opportunity that exists today.

"You can't refinance a home you never purchased."

The Question Worth Asking

Instead of: "Did I miss the 5s?"

Ask: "Does today's payment work for me?"

If the monthly obligation fits comfortably within your financial picture and the property meets your criteria, the spread between 6.1% and 5.9% is unlikely to be the deciding variable — and waiting for it to close could cost you far more in opportunity than it saves in interest.

One more thing worth remembering: mortgage rates are not permanent fixtures. Refinancing is always on the table when conditions improve. But you cannot refinance a home you never bought.

Perspective on Where We Are

It's easy to forget how much the market has already shifted in buyers' favor. Just over a year ago, mortgage rates were above 7%. Today, they're running in the low 6% range — a meaningful improvement in purchasing power that many buyers are still processing.

If you stepped back from your search when rates were at their peak, this is a reasonable moment to revisit the numbers. Not because conditions are perfect, but because the payment math may already work better than your instincts are telling you.

Bottom Line

The gap between rates in the 5s and the low 6s is real — but it's narrower than most buyers assume. Before concluding that you've missed your window, it's worth running an updated analysis based on where rates actually stand today.

If you're considering a purchase in Los Angeles, Beverly Hills, or the surrounding luxury markets, I'm happy to model the numbers specific to your price range.

Contact Christophe Choo at (310) 777-6342 or [email protected] for a Confidential Property Valuation. To tour your future home and search communities, click "HERE".